Last week, Greater Vancouver Realtors (GVR) released its 2024 second-half (H2) housing forecast, which reviews new dynamics impacting the market along with economic trends that informed the first half of 2024.

Here are some highlights of what GVR expects for the second half of the year.

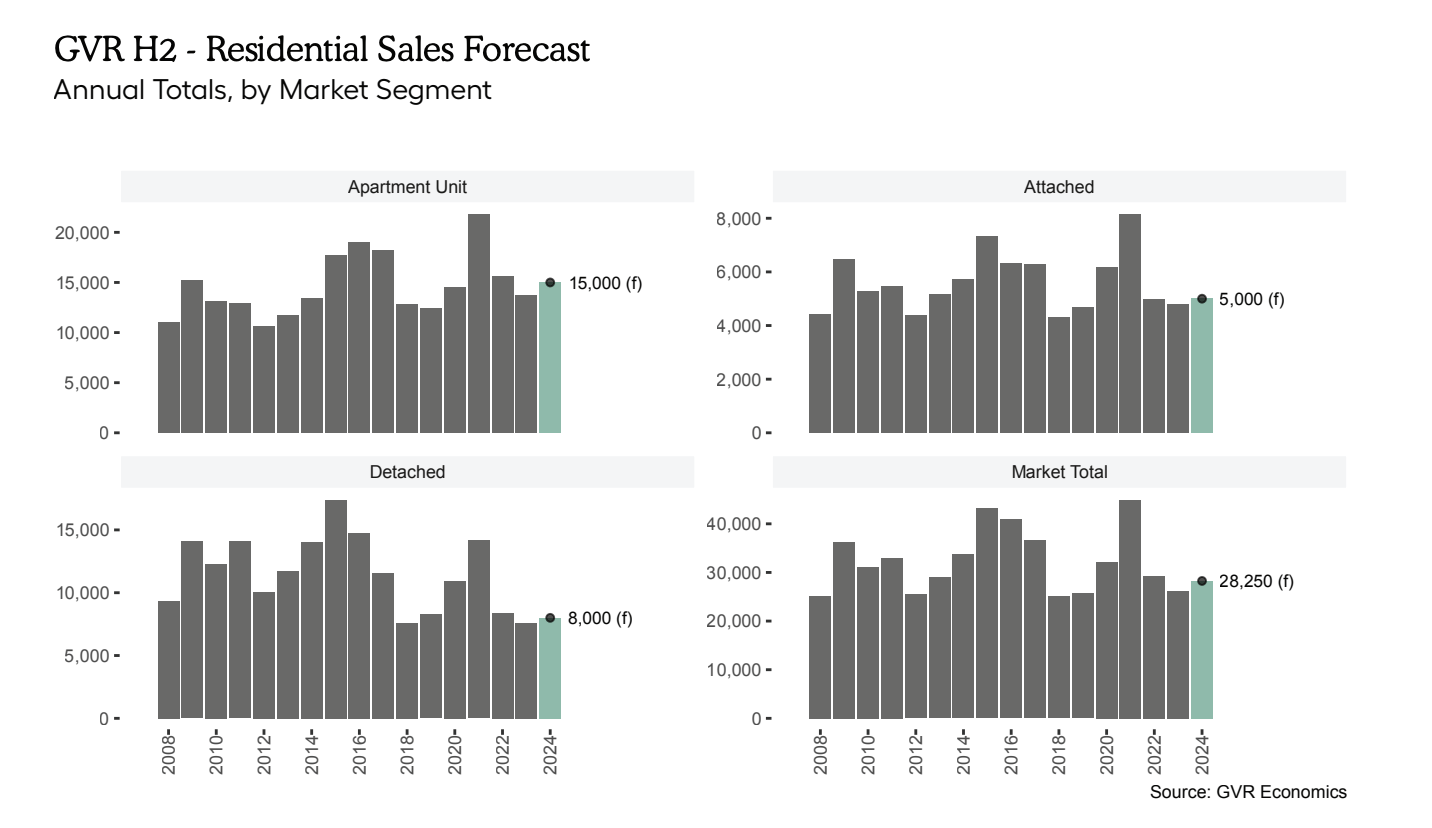

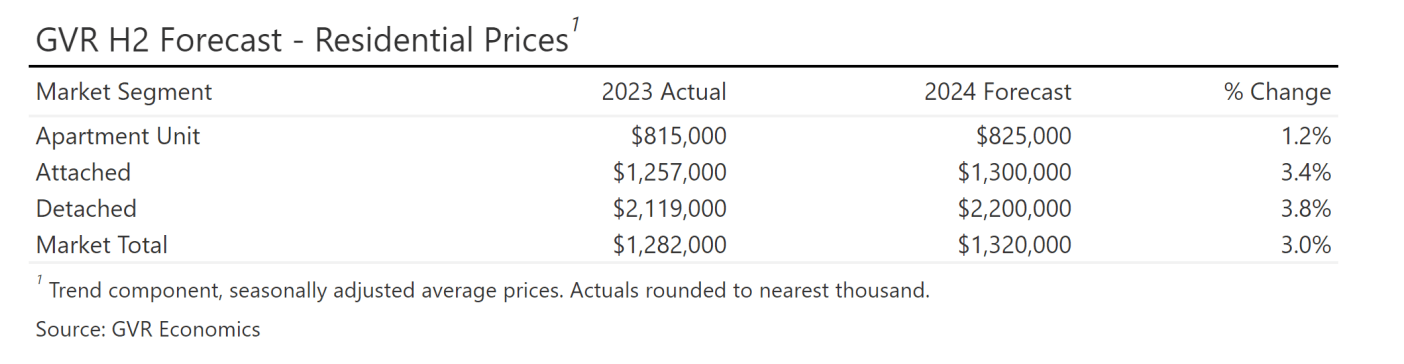

Sales and price forecasts

This year, GVR sales and price forecasts are almost exactly on target, but market balance has shifted from favouring sellers at the year’s start towards more balanced conditions.

GVR’s 2024 first-half (H1) forecast predicted that sales across Greater Vancouver would jump by about 8.0 per cent compared to 2023 (28,250 by year-end).

Sales from January to July this year totalled 16,227, with the prediction being 16,256 — a 0.18 per cent difference. GVR is keeping its year-end sales prediction as-is.

So far, aggregate price metrics have shown slight increases as the H1 forecast predicts, driven by steady sales combined with near-record-low inventory levels at 2024’s start. With these levels rising throughout the past few months, most aggregate price metrics are trending sideways or slightly downward.

Yet the median differential between the list price and sale price for all GVR properties has trended at a close to 2.0 per cent discount since the start of the year.

In the near term, GVR’s outlook for the year’s second half is a balanced market that continues to support modest price appreciation by year-end. The organization keeps its outlook of price appreciation in the 1.0-4.0 per cent range across market segments to year-end.

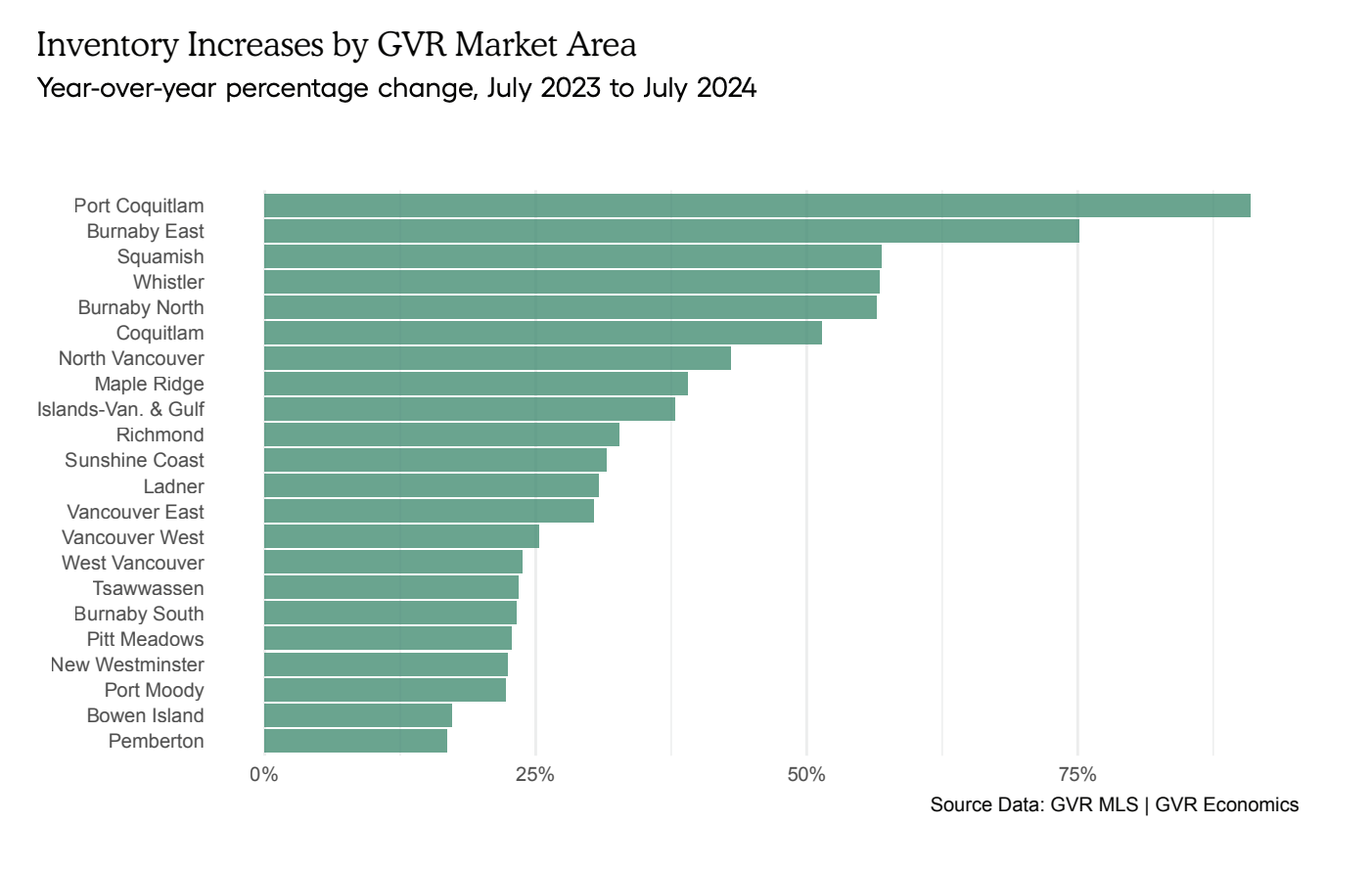

Inventory

As sellers stay keen to list their properties, Greater Vancouver hasn’t seen such inventory level highs since 2019. Compared to 2023 levels, this boost has been the biggest surprise in H1 data.

The main drivers behind this trend are a result of steady demand from buyers along with higher-than-expected new listing activity levels, which isn’t of concern to GVR right now. The sense is that increased inventory might be positive, especially for buyers, as it signals a return to more balanced market conditions.

Though sales are below their 10-year average, they’re not the lowest seen before and this isn’t a new trend. Newly listed properties are meeting or exceeding historical averages, which has resulted in accumulated inventory thanks to below-average sales.

GVR found that many factors have contributed to the new listing activity boost, including the fact that early 2023 had lower-than-normal new listing activity and sellers who waited to sell then are possibly doing so this year.

Interest rate cut impacts

GVR says that while additional reductions to the Bank of Canada’s policy rate are expected this year, it may take longer to see increased buyer demand.

This is suggested by the fact that while the H2 forecast favours another 50-basis point reduction to the policy rate, buyers showed a lack of response to the 50-basis point reduction in H1.

Review the full H2 forecast here.